Alloy

Founded Year

2015Stage

Series C - II | AliveTotal Raised

$208.92MValuation

$0000Last Raised

$52M | 3 yrs agoRevenue

$0000Mosaic Score The Mosaic Score is an algorithm that measures the overall financial health and market potential of private companies.

-15 points in the past 30 days

About Alloy

Alloy provides identity verification and fraud prevention solutions within the financial services sector. The company offers a platform that supports decisions for onboarding, fraud monitoring, and anti-money laundering (AML) processes, as well as credit underwriting. Alloy serves banks, credit unions, and fintech companies. It was founded in 2015 and is based in New York, New York.

Loading...

ESPs containing Alloy

The ESP matrix leverages data and analyst insight to identify and rank leading companies in a given technology landscape.

The alternative credit scoring market addresses the issue of creditworthiness assessment for individuals with thin-files or no file with credit reference agencies. This market provides solutions that allow lenders to accept more applicants by taking into account additional data sources, such as rent or utilities payments, online activity, employment history, or online purchase behaviors. Companies…

Alloy named as Challenger among 15 other companies, including Equifax, Experian, and TransUnion.

Alloy's Products & Differentiators

Licensing fees

Licensing fees for products or use cases purchased

Loading...

Research containing Alloy

Get data-driven expert analysis from the CB Insights Intelligence Unit.

CB Insights Intelligence Analysts have mentioned Alloy in 5 CB Insights research briefs, most recently on Mar 14, 2024.

Mar 14, 2024

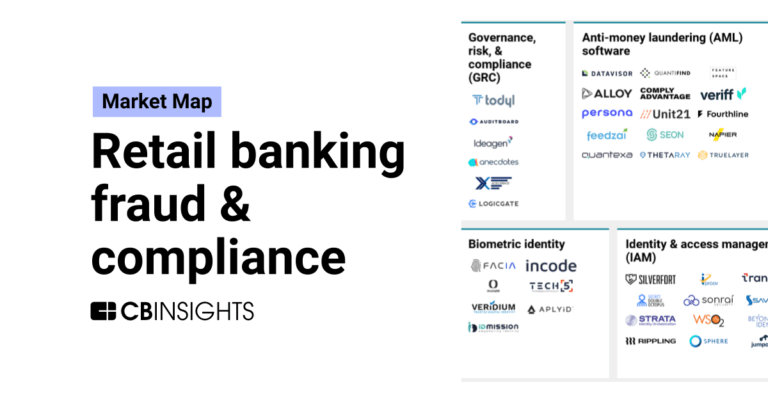

The retail banking fraud & compliance market map

Jan 4, 2024

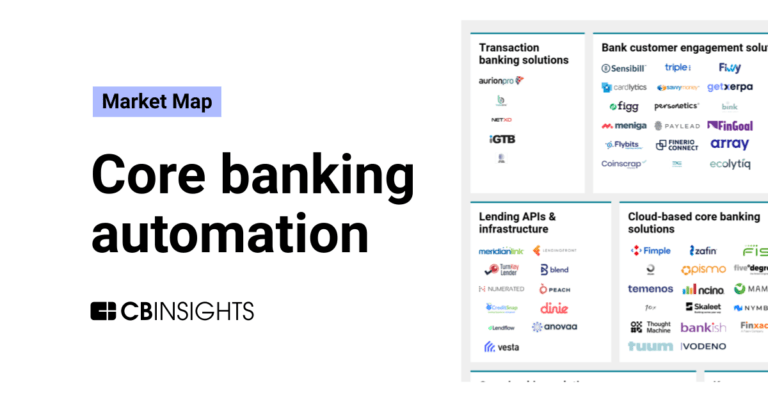

The core banking automation market map

Expert Collections containing Alloy

Expert Collections are analyst-curated lists that highlight the companies you need to know in the most important technology spaces.

Alloy is included in 7 Expert Collections, including Unicorns- Billion Dollar Startups.

Unicorns- Billion Dollar Startups

1,309 items

Regtech

1,921 items

Technology that addresses regulatory challenges and facilitates the delivery of compliance requirements. Regulatory technology helps companies and regulators address challenges ranging from compliance (e.g. AML/KYC) automation and improved risk management.

Digital Lending

2,735 items

This collection contains companies that provide alternative means for obtaining a loan for personal or business use and companies that provide software to lenders for the application, underwriting, funding or loan collection process.

Fintech

9,809 items

Companies and startups in this collection provide technology to streamline, improve, and transform financial services, products, and operations for individuals and businesses.

Fintech 100

849 items

250 of the most promising private companies applying a mix of software and technology to transform the financial services industry.

Digital ID In Fintech

268 items

For this analysis, we looked at digital ID companies working in or with near-term potential to work in fintech applications. Startups here are enabling fintech companies to verify government documents, authenticate with biometrics, and combat fraudulent logins.

Latest Alloy News

Nov 3, 2025

By PYMNTS | November 3, 2025 | Highlights Huntington National Bank, in partnership with Alloy, is launching a corporate venture studio focused on customer-centric innovation—prioritizing real-world needs over trendy technologies. The bank’s approach blends traditional banking strengths like trust and regulatory rigor with agile, startup-like methodologies to co-create solutions alongside customers and fintech partners. Huntington emphasizes purpose-driven strategy: solving genuine customer challenges first, with financial results seen as a natural outcome of meaningful impact and long-term community value. Today’s financial institutions aren’t racing to adopt the latest technology for bragging rights. Instead, they are homing in on the customer journey as the benchmark of meaningful change Get the Full Story Complete the form to unlock this article and enjoy unlimited free access to all PYMNTS content — no additional logins required. yesSubscribe to our daily newsletter, PYMNTS Today. By completing this form, you agree to receive marketing communications from PYMNTS and to the sharing of your information with our sponsor, if applicable, in accordance with our Privacy Policy and Terms and Conditions . Δ “We just want to continue solving problems for our customers,” Igor Cerc , Chief Enterprise Strategy Officer & Head of Ventures at Huntington National Bank , told PYMNTS. “Customers tell us they have a number of real-world problems, and we want to get close to that. It’s how we end up co-creating solutions in the marketplace.” This represents a first-principles level pivot. Historically, banks and financial service providers have adopted new technologies in bursts, reactive phases of digitization that were frequently triggered by competitive threats or regulatory pressure. The knee-jerk response was often to chase the most talked-about tools: blockchain for settlements, AI for underwriting, chatbots for service optimization. For the 150-year-old Huntington National Bank, customer-centric innovation reframes the strategic question from “What can this technology do?” to “What does the customer actually need?” “If we can find the right types of solutions that meet our customers’ needs on the outside, we will partner or we’ll buy. If it means that we need to build, we might build it internally, we might build it through a NewCo or a spin-out,” explained Cerc. That posture represents a large part of the reason why Huntington Bank and Alloy Partners on Oct. 23 announced the launch of a new corporate venture studio. Advertisement: Scroll to Continue Old-World Trust Meets Startup Agility Banks today are not merely mimicking startups; they’re increasingly integrating agile methodologies into their core. And while the conversation around FinTech is too often dominated by technology-first thinking, that’s a trend Cerc is keen to challenge. “We’re not being dogmatic about technology at all,” he said. “Technology plays a big role, but frankly, if we can do it with simple processes and products, so be it.” This focus on simplicity is part of what makes Huntington’s innovation approach stand out. The bank has built a roadmap that intentionally marries its traditional strengths of trust, scale, and regulatory rigor with the innovation playbook of a startup: agile development, rapid iteration, and customer-centric design. “When we say that we want to act more like a tech company,” Cerc explained, “it just means that we want to continue on that agile front.” “We are a bank. We are proud of our discipline and execution,” he added. Still, this hybridization is a cultural as much as a technical shift. Institutions must unlearn top-down command structures and embrace a mindset where failure is not a risk to be minimized but a source of insight to be leveraged. Purpose as a Strategic Compass By becoming co-creators, banks are no longer playing the role of a distant lender but a strategic partner who shares risk, expertise, and upside. This has significant implications for speed-to-market. A FinTech developing a new payments app can now prototype directly with a banking partner rather than waste months securing permissions. Meanwhile, the bank gains exposure to cutting-edge tech and new customer segments without bearing full R&D costs. “We are evolving from being that capital provider to a co-creator and a platform for innovation,” Cerc said. “Our focus right now, and how we think about success, is can we actually solve real customer problems in a meaningful way and contribute to our communities broadly,” he added. “The financial results follow from that.” For all its promise, customer-centric innovation is not a plug-and-play strategy. It demands long-term investment, cultural alignment, and clarity of purpose. Customers are increasingly skeptical of superficial gestures or opaque intentions. To win trust in a disintermediated, data-saturated world, institutions must communicate not just what they’re building, but why. Rather than innovation for its own sake, the focus always returns to the fundamental role of banking: solving real-world problems for real people, at scale. For its part, Huntington Bank has built out a roadmap for the next six months and is approaching the effort with methodical discipline. Yet Cerc admits there’s still considerable white space, and that’s intentional. Asked if he has a wish list of ideal companies or capabilities the bank hopes to attract, Cerc replied: “Not specifically. We have a systematic approach … going customer segment by customer segment. They will take us where the world will take us.” Igor Cerc, is chief enterprise strategy officer and head of ventures at Huntington National Bank and a senior strategy and innovation executive who has led $1.5B in acquisitions, launched four startups, and serves on two FinTech boards. Recommended

Alloy Frequently Asked Questions (FAQ)

When was Alloy founded?

Alloy was founded in 2015.

Where is Alloy's headquarters?

Alloy's headquarters is located at 41 East 11th Street, New York.

What is Alloy's latest funding round?

Alloy's latest funding round is Series C - II.

How much did Alloy raise?

Alloy raised a total of $208.92M.

Who are the investors of Alloy?

Investors of Alloy include Bessemer Venture Partners, Avid Ventures, Felicis, Canapi, Lightspeed Venture Partners and 23 more.

Who are Alloy's competitors?

Competitors of Alloy include AuthenticID, Sardine, Lendflow, Persona, Worth and 7 more.

What products does Alloy offer?

Alloy's products include Licensing fees and 3 more.

Who are Alloy's customers?

Customers of Alloy include Mountain America Credit Union, Live Oak Bank, Suncoast Credit Union, Ramp and Stash.

Loading...

Compare Alloy to Competitors

Unit21 offers a no-code platform for risk and compliance operations within the financial services sector. The main offerings include tools for preventing and detecting payment fraud, monitoring anti-money laundering (AML) transactions, and providing device intelligence and customer risk ratings. The platform includes features such as artificial intelligence (AI) driven alerts, case management, regulatory filing automation, and risk data enrichment. It was founded in 2018 and is based in San Francisco, California.

Sumsub operates as an identity verification platform serving the fintech, crypto, transportation, trading, e-commerce, and gaming industries. The company offers services such as user verification, business verification, transaction monitoring, and fraud prevention, powered by artificial intelligence (AI) to support compliance and security. Sumsub provides tools, including document and biometric verification, as well as anti-money laundering (AML) transaction monitoring, and analytics for risk scoring and case management. It was founded in 2015 and is based in London, United Kingdom.

Veriff provides identity verification services within the cybersecurity sector. The company offers services such as identity and document verification, proof of address, database verification, age validation, Anti-Money Laundering (AML) screening, biometric authentication, and fraud prevention. Veriff serves sectors that require identity verification processes, including financial services, e-commerce, iGaming, video gaming, mobility, transportation, and human resources. It was founded in 2015 and is based in Tallinn, Estonia.

Persona provides identity verification and compliance services within the financial technology sector. The company offers a platform that automates know your customer (KYC), anti-money laundering (AML), and know your business (KYB) programs, as well as fraud prevention, by collecting and verifying personal information for various use cases. Persona's services include case reviews and orchestrating custom rules and third-party data integration. It was founded in 2018 and is based in San Francisco, California.

Trulioo provides identity verification and fraud prevention within the digital economy. Its services involve verifying identity documents and business entities, as well as checking against global watchlists. Trulioo serves sectors that require identity verification solutions, such as financial institutions and e-commerce platforms. It was founded in 2011 and is based in Vancouver, Canada.

Middesk operates as a business identity platform that provides onboarding, underwriting, and compliance support specifically for financial services. The company offers services including business verification for know your business (KYB) compliance, risk management, credit assessments, lien filing, and payroll tax registration. Middesk serves sectors such as banks, fintechs, lenders, and marketplaces. It was founded in 2019 and is based in San Francisco, California.

Loading...